What is a Real Estate Investment Trust (REIT)?

Published on Feb. 20, 2013

A Real Estate Investment Trust is a corporation that exists for the purpose of acquiring, managing, and selling real estate for the benefit of shareholders. REITs are one of the primary types of investment structures for clients who desire to participate in the potential for income and capital appreciation supported by commercial real estate. This article will help you understand the structure and operations of REITs, the potential benefits and risks of REITs as investments, and the way by which we analyze and filter REITs to generate strong investment recommendations for income and appreciation backed by significant collateral.

Institutional Real Estate

REITs provide individuals with access to income and appreciation derived from both equity and mortgage positions in institutional real estate. REITs are typically structured to pay investors income on an ongoing basis (either monthly or quarterly). Unlike most other types of corporations, which can choose whether or not to distribute a dividend, a REIT must distribute to its shareholders at least 90% of the taxable income produced from either the property rents or the mortgage payments.

REIT Categories

- Non-Traded or Publicly Traded

- Both types of REITs are publicly registered (and thus, provide financial reporting to the SEC, available online to all shareholders on a quarterly and annual basis), but only publicly traded REITs are listed and sold on the stock market.

- Non-traded REITs tend to be fairly illiquid with limited liquidity provisions until the portfolio has been sold or listed on the stock market.

- Publicly trades REITs are generally liquid as their stock trades on the various stock exchanges. Of course, because of this, publicly traded REITs are subject to stock market correlation and risk.

- Equity, Debt, or Hybrid

- Equity REITs participate in income and profits derived from asset ownership and management.

- Mortgage REITs participate in the interest income, fees, and profits derived from buying, originating, servicing, and selling mortgages collateralized by commercial real estate.

- Hybrid REITs participate in both equity and mortgage acquistions and originations.

- Asset-Class-Focused or Diversified

- REITs are able to target specific asset classes or diversify over many asset classes within the same portfolio.

The flexibility of the REIT structure allows investors to be selective of the real estate sectors they want to target, as well as the manner in which they want to invest. Publicly traded REITs tend to trade more expensively than non-traded REITs. Investors can take advantage of this price difference by acquiring non-traded REITs that are structured to eventually list on a public stock exchange. Utilizing this strategy, investors may earn a higher yield and take advantage of the potential profit spread between the private and public markets when a non-traded REIT "goes public." Alternatively, investors can acquire shares at a discount for publicly traded REITs when stock markets decline heavily, taking advantage of the lower price points caused by fear rather than rational valuation.

The flexibility of the REIT structure allows investors to be selective of the real estate sectors they want to target, as well as the manner in which they want to invest. Publicly traded REITs tend to trade more expensively than non-traded REITs. Investors can take advantage of this price difference by acquiring non-traded REITs that are structured to eventually list on a public stock exchange. Utilizing this strategy, investors may earn a higher yield and take advantage of the potential profit spread between the private and public markets when a non-traded REIT "goes public." Alternatively, investors can acquire shares at a discount for publicly traded REITs when stock markets decline heavily, taking advantage of the lower price points caused by fear rather than rational valuation.

Passive

REITs allow individual investors to access and rely upon the expertise provided by institutional asset management firms for all decisions regarding the real estate portfolio. REITs are passive investments, structured to provide acquisitions, property management, dispositions, investor communication, and the distribution of investors' income produced from the portfolio.

Tax Benefits and Total Return

Due to the unique structure of REITs, corporate taxes are reduced or eliminated, which increases the income that can be paid as a dividend to investors. Additionally, REITs are able to pass through depreciation tax shelter of the real estate portfolio to individual shareholders, thus allowing shareholders to defer taxes on current income. REITs do not qualify for a 1031 exchange unless an UPREIT structure is utilized.

The total return of a REIT is comprised of 1) the income received from the portfolio of real estate assets added to 2) potential appreciation realized upon the disposition of the assets in the portfolio.

Important Considerations

While we love the concept and structure of a REIT as an investment, there are actually very few REITs that make it through our strict due diligence to become investments for us and investment recommendations for our clients. As a market segment, publicly traded REITs are currently overvalued (generally speaking) and we tend to reject 95% or more of the non-traded REITs that are available at any given time.

While we love the concept and structure of a REIT as an investment, there are actually very few REITs that make it through our strict due diligence to become investments for us and investment recommendations for our clients. As a market segment, publicly traded REITs are currently overvalued (generally speaking) and we tend to reject 95% or more of the non-traded REITs that are available at any given time.

For publicly traded REITs, we await market crashes or sector specific declines before making and recommending investments in this area in order to achieve higher dividend income, lower downside potential, and higher appreciation potential. As of Feb 2013, publicly traded REITs are very expensively priced due to the mad dash for yield by income-starved investors. Since the Fed is keeping interest rates so abnormally low, investors are looking for income wherever they can get it and REITs are a well-known source of monthly or quarterly income.

On the non-traded side of the equation, we have found that there are only 1-3 REITs per year out of 50-60+ that we can recommend to our clients and into which we invest our own capital. We reject the other 95% of available non-traded REITs for a number of reasons we will highlight below.

What to Watch Out For

REITs are collateralized by commercial real estate and therefore, are not immune to many of the risks that are associated with real estate investing. More specifically, each REIT investment is subject to the risks of the markets, asset classes, acquisitions, structure, management, and financing that are particular to the portfolio of real estate owned by the REIT.

REITs are collateralized by commercial real estate and therefore, are not immune to many of the risks that are associated with real estate investing. More specifically, each REIT investment is subject to the risks of the markets, asset classes, acquisitions, structure, management, and financing that are particular to the portfolio of real estate owned by the REIT.

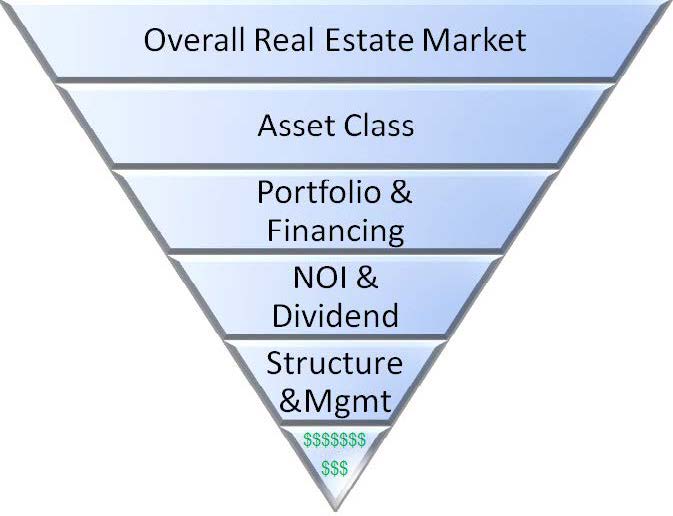

These are the primary considerations/risks that we take into account before making a REIT investment or recommendation:

- Where are we in the overall real estate/economic market cycle?

- This a macroeconomic question regarding general investment timing for the overall real estate market. In 2005-2009, it was very difficult to find many good REITs because the overall market had become overstretched and overvalued. In the past couple of years and over the next 12-24 months, REITs have made a lot more sense as a general investment category because of the large drop in prices from peak levels in 2005-2007.

- This is in no way a blanket endorsement of all REITs, but it does make it a little easier for more REITs to be attractive since the discounts in the real estate market have been extremely broad.

- Where are the asset classes in their respective valuation cycles?

- This question narrows the focus from the overall real estate market to specific asset classes. Each asset class, like stock market sectors, may act somewhat independently under normal market circumstances.

- For example, multifamily has been benefiting from the mass exodus of the US population fleeing to rent vs. own after the Great Recession and the willingness of government agencies to provide easy financing for this asset class, fixed at 3-4% for 30-40 years. For value-oriented investors, this asset class is no longer very favorably priced due to these demographic and financing trends. That is not to say there are not deals to be had in this asset class, but the discounts are few and far between.

- Since many REITs are asset-class specific, understanding the broader asset class valuations can aid investors in avoiding those REITs that may be targeting a generally overvalued category.

- What is the quality and value of the ultimate collateral (properties) of the REIT and the REIT's income?

- REITs are not "guaranteed" investments. The income, downside protection, and upside potential are derived from the properties in the portfolio.

- In general, we analyze each property acquisition in a REIT (sometimes in the multiple hundreds of properties per portfolio!) to determine if the properties are well-located, bought at a reasonable or value-oriented price, meet the overall direction of the REIT, and fall within the scope of the REIT's management experience and expertise.

- The dividend paid by a REIT is not guaranteed by the REIT management, but rather is derived from the performance and income of the underlying properties in the portfolio.

- If the incomes from the individual properties of a portfolio are reliable and purchased opportunistically, this will ensure a more stable dividend to shareholders and a longer-term value for future potential sale profits.

- Considering the macroeconomic perspective, understanding the specific sources of a REIT's income allows an investor to better prepare for downside protection or inflation hedging.

- For example, some REITs primarily comprise investment grade net-leased properties. The lease guarantees that back the income for these types of properties may be more dependable due to the credit strength of the underlying tenants and the longer-term nature of the leases.

- If an investor is seeking an inflation or demographic hedge, they could target REITs focused on healthcare or senior care.

- Is the REIT near closing the capital raise (i.e., likely no longer a blind pool)?

- REITs generally remain open to new investors for a period of 1-3 years. Most REITs maintain the same share price for new investors throughout their entire capital raise. In the meanwhile, as they raise capital, they typically make acquisitions on a regular basis. Thus, instead of investing early into what is basically a blind pool, an investor could wait until the very end of a REIT's capital raise to determine the quality of the portfolio, management, dividend coverage, etc. up through that point.

- Waiting until closing and capital placement not only significantly reduces risk, but it also provides a much better internal rate of return since an investor would not have to wait as long to benefit from a potential "full cycle" event (i.e., when a REIT's portfolio is listed on a stock exchange or when its portfolio is sold).

- Is the dividend paid to investors being fully covered by the net Cash Available for Distributions (CAD)?

- It is imperative that a REIT cover the dividend it pays to shareholders with actual net cash from operations available for distributions.

- Most REITs we reject partially finance the dividend that they pay to investors, inflating the distributions at the expense of investors' long-term value.

- Due to the large scale operations and expenses that are involved in running, managing, and accounting for a REIT, most REITs must reach a size of approximately $200-$400 million in assets before dividend coverage is well within reach.

- Many REITs do not ever reach dividend coverage prior to the close of their capital raise due to their ongoing fees, lack of income, or property underperformance. In some cases, the REIT advertised a dividend that may not have ever been within its reach, setting investors up for disappointment (due to lower income) once it closes its capital raise.

- We reject Funds From Operations (FFO), Modified Funds From Operations (MFFO), and Adjusted Funds From Operations (AFFO) calculations that allow for creative financing and expense accounting for dividend coverage. Instead we use CAD. The bottom line question for us is quite simple. Does the portfolio of property actually cover its own dividends with actual cash or not? It is very RARE for relatively new REITs to reach full dividend coverage prior to closing to new investors.

- Is there a large amount of debt or lease rollover coming in the short-term or any other major potential portfolio negatives on the horizon?

- In keeping with analyzing the sustainability of income, it is important to understand the amount of debt a REIT has outstanding and when that debt comes due. If there is a large portion coming due at any one time, it is imperative to know whether the REIT has the capital and portfolio quality to get that debt refinanced.

- It is much more secure to deal with REITs that either have very low to moderate leverage, or that have very long-term fixed financing to ensure a long enough time span to go through various market cycles.

- The same concept applies to lease rollover for portfolios that depend on office, retail and industrial tenants for their net operating income.

- What is the exposure to interest rate risk?

- What portion of the portfolio's financing is subject to long-term fixed vs. short-term or floating-rate debt? Floating-rate and short-term debt may be less expensive than long-term financing, but the interest rate risk may not be worth the short-term benefit. Inflationary pressures could push interest rates higher and therefore the REIT's income lower on a more permanent basis.

- Management Experience and Alignment with Investors

- Does the incentive structure for the REIT sponsor/manager align their interests with investors?

- Are they motivated for profit on the backend which would encourage them to seek as profitable a growth and exit strategy as possible?

- OR are they compensated with large upfront and ongoing management fees that encourage them to hold the portfolio indefinitely because of the amount of money they make from management (vs. selling)?

- Does the management of the REIT have experience with the asset class or classes they are targeting?

- Does the management of the REIT have experience with large scale investment real estate portfolios and seeking profitable exit strategies? It is one thing to have experience with a type of asset. It is quite another to manage a multi-billion dollar portfolio or real estate to be eventually sold or listed on the stock market.

Recommendations

Recommendations

Given the vetting process listed above, it is probably not hard to see why so few REITs make the cut. The good news is that 1-3 REITs do make it through our rigorous vetting process each year, and these select few have turned out to be stellar investments for our clients, both in terms of income and appreciation.